This informal CPD article Understanding Debt was provided by WiseAlpha Technologies, the UK's leading digital bond market giving private investors access to the world of corporate bonds. When it comes to understanding how bonds work, getting to grips with debt is crucial. Because this field can be jam-packed with jargon, having a working knowledge of the key terms can help you make serious strides in your journey to master the world of bonds.

Secured Debt

Let’s start with all things related to secured debt! Secured debt offers protection against a company's assets or cash flows. This form of secured debt is typically offered at the OpCo level, where the assets and cash flows are closest. In this case, the bond documentation contains a set of rules, or covenants, that regulate how the security will be enforced.

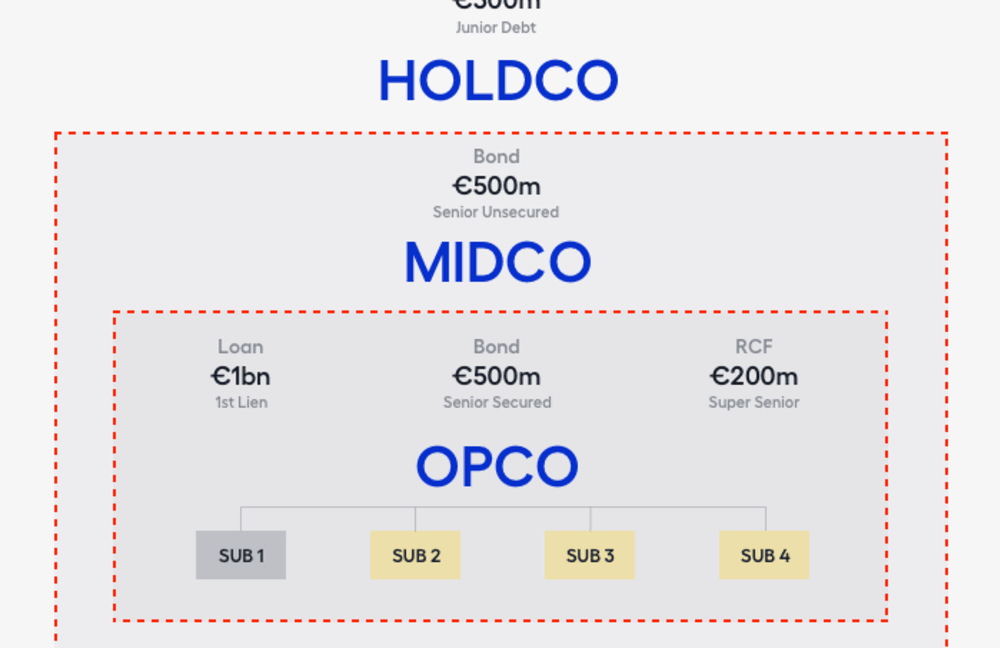

The OpCo has four subsidiary companies, as shown in the HYL structure below. The “guarantors” of the debt issued at the OpCo are the ones in yellow. The “restricted” entities are the guarantor subsidiaries. They're "restricted" since they're used as collateral for OpCo bonds, which means the secured claim restricts their assets and cash flows.

A "Restricted Group" is formed by these subsidiaries and the issuing corporation. This is shown as the red dotted line. One way to think of a restricted group is that it has a fence surrounding it. The fence stops assets or cash flow leaving the restricted group before it is applied to pay down debt or the company has met certain tests. What is also worth noting is the availability of a revolving credit facility (RCF), which are essentially funds made available by lenders for the day-to-day operation of the business – similar to a corporate overdraft. RCFs are typically senior secured but will generally be more senior in some respects than senior secured debt - it is often one class of debt that is considered “super senior” for reasons we will touch on later.

Leveraged Loans

A type of senior debt is known as leveraged loans, these types of loans are often senior secured loans sold as part of a big ‘Credit Facility' in a syndicated procedure. This Credit Facility is usually composed of a Revolving Credit Facility (RCF) which is a loan that can be drawn down like an overdraft. Then there are usually “tranches” or additional loans. These "term loans" have a specified maturity and are typically secured by a first lien or claim on assets or cash flows, making them senior secured. Second and third lien loans are possible, but they will be junior to the liens that come before them.

Term loans are either amortising or have a bullet payment. Unlike bonds, they do not have a call structure. Amortizing "Term Loan A"s feature an amortisation schedule that gradually reduces the outstanding debt. The syndicating banks normally own these, as well as the RCF. “Term Loan B”s, where B stands for "Bullet”, loans are usually purchased by institutional investors. These loans however don’t have an amortisation schedule unlike "Term Loan A"s

Loans have a floating interest rate, less liquid than bonds, and can be repaid at any time. Within a given credit facility, there might be many loans. Historically loans were private instruments, but more are now traded publicly, the majority do however largely remain private. A necessity in this context is a confidentiality agreement in place between issuer and lender. Loan investors would typically receive monthly financial reports from the issuer as well as comprehensive financial projections. This agreement for constant communication and increased information allows for lower funding costs, but it is commercially sensitive and hence must be kept "private."

When an issuer has outstanding high yield bonds, they can choose to issue loans in a “public” fashion, in which case bond and loan holders receive the same information, or in a “private” manner, in which case bond holders will be at a disadvantage in terms of information.

HYL’s Secured Debt

A €1,000 Term Loan B and a €500mm Senior Secured Bond make up HYL's senior secured debt. They profit from the collateral guarantees provided by the restricted group's subsidiary companies.

In terms of security, the RCF is commonly referred to as "pari passu," or of equal footing. The RCF, on the other hand, is normally owned by the syndicating banks, and the bond documentation specifies that the RCF receives priority in terms of repayment. It is also important to note that covenants apply to RCF, Loans, and Bonds alike. The RCF normally has the strictest covenants, as there is always a maintenance covenant that must be followed when drawing some or all of the RCF.

Loan Covenants

Loan covenants have weakened over time but are generally stricter than high yield bond covenants. Maintenance covenants can be imposed on loans, requiring that excess cash flow be utilised to pay down debt. Incurrence-based covenants control high-yield bonds, and they are tested when an event occurs. Understanding what covenants apply across the capital structure is critical in a stressed/distressed situation. For example, if an issuer relies on being able to draw funds from an RCF to fulfil interest payments or deal with a liquidity squeeze, it's critical to understand the parameters under which this is or is not achievable.

RCF and loan covenants, on the other hand, may not be disclosed. If RCF or loan maintenance covenants are broken, instead of demanding repayment of the RCF or loan, holders may elect to "waive" the covenant breach in exchange for a fee or a higher coupon rate on their investment. If lenders require repayment, this is known as a "cross default." When one class of debt defaults, the “Cross Default” clause normally states that all debt is in default. Lenders are protected across the capital structure as a result of this. Because the cross default clause can exclude some types of debt; it's then crucial to determine if your bonds are covered.

HYL has unsecured debt issued through a holding company named MidCo in addition to debt issued at the OpCo level. MidCo has issued €500m of senior unsecured bonds. These bonds have security over the equity of MidCo. MidCo's only asset is its ownership of OpCo in this context.

A restricted group also includes senior unsecured bonds. MidCo's ability to pay interest on its bonds is reliant on cash flow from OpCo. This means that any repayment revenues after the senior secured debt has been repaid benefit them on an unsecured basis.

Covenants controlling the senior secured group, as well as covenants defining unsecured bondholders' rights in relation to senior secured and more junior debt holders, apply to this secondary restricted group. This secondary restricted group is subject to covenants governing the senior secured group; as well as covenants that set out unsecured bond holders' rights relative to the senior secured and more junior debt holders.

Borrowing Base Loans

Borrowing Base Loans are a collateralised form of secured lending that you may see. The size of the amount the issuer can borrow is tied to the value of an asset on the balance sheet. Lenders require that the value of the assets backing the loan be examined on a regular basis, and that if the value is deemed to have changed, the size of the available loan be adjusted accordingly. An issuer, for example, could lend against its receivables. In this situation, the lender will over-collateralize the loan by lending a fraction of the total assessed asset value, then collecting receivables and paying down the loan with each one collected. The more illiquid the asset the greater the collateralisation hence lenders will normally lend a lesser percentage against inventories than receivables collected. Borrowing base loans represent additional claims or liens on specific assets.

Mezzanine Loans

Now let’s move on to what is known as Mezzanine Loans. These are effectively unsecured loans, or at least 2nd Lien loans. They are the equivalent to unsecured high yield bonds. And in terms of coupon they have cash pay and “PIK” components (see later).Mezzanine loans often have shorter call periods than high yield bonds, giving the issuer a little more flexibility. Equity warrants are sometimes tied to mezzanine loans. The warrants allow the lender to share in the equity gains while also compensating for the additional risk associated with subordination. Generally, mezzanine issues are associated with all loan or smaller transactions. Larger transactions see a mixture of loans and high yield bonds being issued.

Before we look at the most junior lenders in HYL’s capital structure we should talk about the intercreditor agreement. At this point, it should be clear that the number of investors who can participate in a high yield issuer can be rather substantial. When you consider that high yield issuers may be able to borrow not only from banks, loan and bond holders, but also from investors across several locations, the number and variety of investors grows significantly. An “intercreditor agreement” is a document which sets out the priority of repayment to all lenders as well as a timeline for resolution in the event of a default.

Payment in Kind (PIK) Bonds

HYL’s most junior debt is its Payment in Kind (PIK) Bonds. These sit outside both restricted groups. PIK bonds are bonds which instead of paying a coupon wholly in cash will pay all or a large part of interest due in the form of additional principal (debt).For example, instead of paying 10% interest on the loan amount, a PIK with a 10% coupon will grow in size by 10% each year. PIK bonds conserve cash and reduce the tax bill as the “interest” payment reduces profit before tax. Because they are frequently highly subordinated and hence akin to equity, PIK bonds are considered aggressive instruments. Because interest is not paid and instead accrues in the form of increasing notional, investors are only compensated when the PIK Notes mature or are called. PIK bonds can have a partial cash pay coupon or only pay cash when funds are available to fulfil the payment or when certain conditions are met. An oil business, for example, might only pay coupons in cash if oil prices are over a specific threshold. The bond is known as a PIK "Toggle" when the coupon can flip between cash and notional accrual.

The PE group, which owns HYL, has invested €700 million on the acquisition. Owners are rewarded in the end when they "Exit," or sell the firm for a greater price to another company in the same industry or list it on the stock market via an IPO.

From secured debt to leveraged loans there are lots of factors to consider and make note of for both the lender and issuer. A smooth and transparent process is ensured by being aware of these all these contingencies.

We hope this article was helpful. For more information from WiseAlpha Technologies, please visit their CPD Member Directory page. Alternatively please visit the CPD Industry Hubs for more CPD articles, courses and events relevant to your Continuing Professional Development requirements.